It has been nearly a year since the coronavirus pandemic upended the world. Every element of our lives has shifted as a result. Work and personal relationships take place via video conferencing. Shopping happens online, with pickup curbside. Social engagements are a fond, distant memory – and banking has shifted online or to mobile devices.

To be fair, elements of the before times do still exist. Bank branches are occasionally open, and consumers can schedule time to come in and have their financial needs met. But as industry expert Jim Marous notes in a recent post for The Financial Brand, “the impact of change was accelerated exponentially during 2020, with digital engagement and technological advancements advancing years in a matter of months. In the last twelve months, banks that successfully pivoted to a digital-first business model were rewarded with improvements in “customer acquisition results, efficiency ratios, customer satisfaction improvements, and overall digital maturity.”¹

In the last twelve months, banks that successfully pivoted to a digital -first business model were rewarded with improvements in “customer acquisition results, effeciency ratios, customer satisfaction improvements, and overall digital maturity.”¹

Revving Up Evolution

The incredible pace of change is one of the key themes that consultancies, analysts and practitioners all acknowledge. Jamie Warder, Executive Vice President and head of digital banking for KeyBank, notes in the ABA Banking Journal: “We’re seeing years of adoption in a matter of weeks.” For many banks, the rapid acceleration of digital transformation has become a make-or-break moment, where those with the vision and means to hit the ground running are going to leave slower, less nimble organizations behind.

In the last twelve months, banks that successfully pivoted to a digital-first business model were rewarded with improvements in “customer acquisition results, efficiency ratios, customer satisfaction improvements, and overall digital maturity.”¹

But that doesn’t mean that every major bank was blazing the trail – only 12% of organizations identified as a digital transformation leader. A majority (64%) identified their companies as fast followers or mainstream players, showing that while many organizations are offering digital services, they are still struggling with embedding end-to-end digital initiatives across the enterprise.

Still, the vast majority of institutions acknowledge that improving digital experiences is a top strategic priority for 2021. The billion dollar question: How can banks quickly evolve and put their best digital feet forward?

Partners in Digital Transformation

One of the fastest, most efficient ways for banks and other financial institutions (FIs) to super-charge their digital transformation initiatives is to partner with a proven solution provider. By tapping into the resources and expertise of a tenured, tested company, FIs can quickly adapt to the shifting market dynamics.

While the list of benefits that come with partnerships are virtually limitless, let’s examine three significant areas where a solution provider like Zoot can drive immediate value.

Digital Onboarding

From a customer acquisition perspective, digital onboarding is an urgent need. As we noted in our recent whitepaper The State of Origination: 2020, almost 64% of checking account applications in 2020 came in via mobile or online channels.[i]

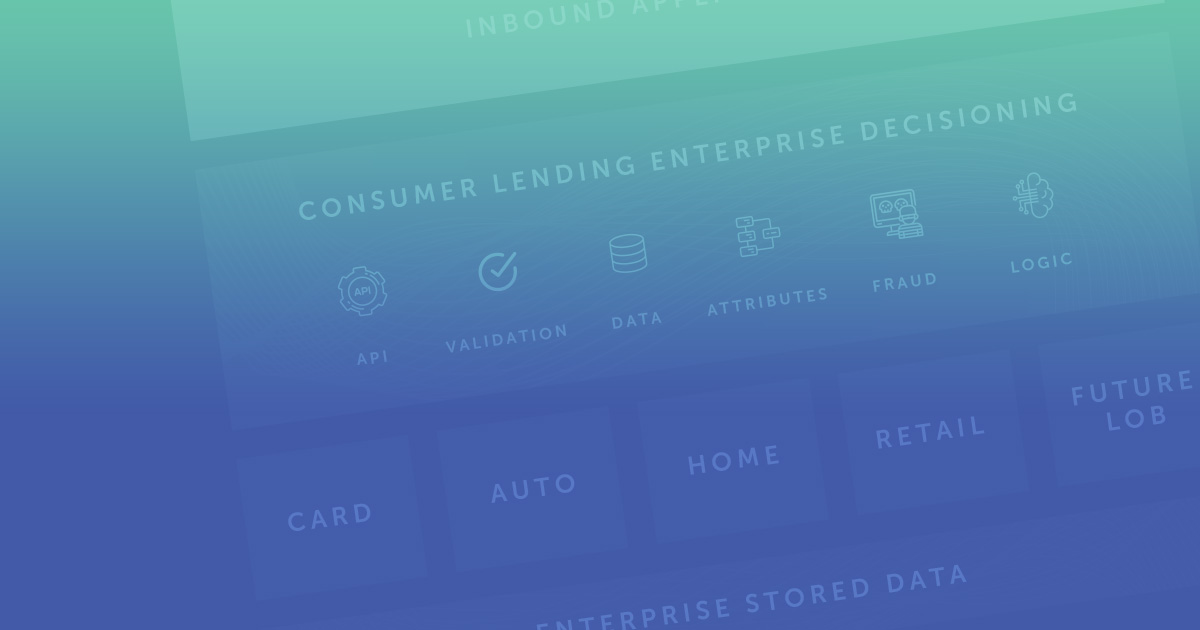

With a digitally-native Instant Decisioning or Origination solution like one from Zoot, FIs can easily and quickly implement digital onboarding processes. From developing application screens that work online and on mobile devices to automating the decisioning process from start to finish, FIs can put powerful digital tools in place to embrace the shift in consumer behaviors.

Using a digital onboarding solution also enables companies to capitalize on the precise moment of customer engagement, regardless of the channel. With front and back-end support that spans an organization’s website, mobile app, branch or call center, Zoot’s solutions let FIs deliver best-in-class experiences with immediate responses and smooth transitions from application to funding.

Underwriting Efficiency

Application experiences are only one element of a comprehensive digital transformation. FIs also face constraints in their underwriting and back office operations, often relying on legacy systems that can limit throughput and internal efficiency.

Many legacy systems have been supporting operations for decades. Hard-coded applications and green screen terminals are still a part of many an underwriter’s day, creating a rigid and challenging environment for underwriters.

Again, this is where the value of a nimble, digital-first partner can pay huge dividends. Using an underwriting solution like Zoot’s, FIs can create modern underwriting workflows and custom screens that radically improve individual efficiencies. Using role-based permissions and automated workflows, banks can increase operating profit and reduce application decisioning expenses.

Best of all, an underwriting solution from Zoot provides companies a future-proof approach to internal digital transformation. FIs will enjoy unlimited scalability and flexibility, with a clean and clear path that supports expansion and growth goals.

Data and Service Acquisition

At the heart of any digital transformation is data. Access to data, and services informed by data, can mean the difference between delightful or devastating customer experiences. Whether an organization is making personalized product offers, executing credit or fraud risk models, experimenting with champion/challenger approaches to growth or looking to expand their offerings in a traditionally underserved population, data is the lynchpin that makes it all possible.

For FIs shackled by legacy systems, bringing in data and acting on it may be close to impossible. Coding and connecting APIs, creating readable data formats, incorporating external data into existing decisioning flows – those tasks can tax even the most seasoned developers, consuming resources and time that are in short supply.

This is simply another example of the value of the right partner. A partner that embodies a data and services acquisition mindset can immediately connect legacy systems with virtually any internal and external data source, allowing companies to put the right data to use when and where they want it.

Zoot is no stranger to data and service acquisition, and provides plug-and-play access to hundreds of data provider products and services. From traditional credit scores to emerging and alternative data; from KYC and ID verification services to predictive analytics; from mobile device authentication to AI and ML inputs, Zoot can empower FIs with the data they need to make the best decisions for the business.

Change Today, Gain Tomorrow

Committing to digital transformation means thinking about both immediate and future impacts. Will today’s approach work in a year? Two years? Five years? If the recent past has taught us anything, it’s that there are no certainties on the road ahead, so companies need to have confidence that their approach can adapt and change to meet the inevitable unknowns of tomorrow.

With Zoot, FIs can confidently tackle the problems of today, knowing that the solutions they have will serve them without fail far into the future. If your organization is ready to take digital transformation to the next level, contact us today.

[1]https://thefinancialbrand.com/106004/banking-review-trends-digital-covid-experience-ai-transformation/

[2] Ibid

[3] https://www.forbes.com/sites/ronshevlin/2020/09/21/new-consumer-research-finds-consumers-open-more-checking-accounts-digitally-than-in-branches