Just over a year ago, the scope and scale of the nascent pandemic was emerging. Alarm bells were going off about the impacts of lockdown and shutdown. As time dragged on, unemployment skyrocketed and fears of mortgage, credit card and loan defaults weighed heavily on creditors – we wrote a couple of posts to that effect (here and here).

To combat the potential tsunami of defaults, both the US government and loan issuers took unprecedented action. Lenders put loans, card payments and mortgages into forbearance for borrowers who could prove economic hardship resulting from pandemic-related job losses or financial impact.

The government issued an initial stimulus payment – then a follow-up payment – and then even more payments and credits. Congress passed additional weekly unemployment payments in addition to the benefits out-of-work Americans received. Consumers took advantage of all these programs as quickly as they became available. The looming wave of defaults quietly settled into smooth and calm waters (for now).

Three of the top card issuers – Discover, Capital One and Synchrony – are reporting card balances down 9%, 17% and 7% in the first quarter from a year prior, respectively.” (iii)

Disappearing Debt

One of the most interesting developments from all this action is the tremendous reduction in consumer credit card debt. Our blog noted that in May 2020, total estimated card debt in the US was approximately $1.07 trillion, with each household owing more than $7,000. This month, the Wall Street Journal reports that “Americans are paying down their credit-card debt at levels not seen in years.”[i]

At the end of March, the estimated outstanding credit card debt for Americans stood at $749 billion. Three of the top card issuers – Discover, Capital One and Synchrony – are reporting card balances “down 9%, 17% and 7% in the first quarter from a year prior, respectively.”[ii]

Experts are chalking up declining debt to a combination of factors, including stimulus, lower spending on things like dining out and traveling, and a reluctance to assume debt in tumultuous times. For consumers, debt reduction means less interest accrual and fewer bills. But for card issuers, it means loss of revenue.

Creating Card Opportunities

To combat the decline in balances, banks are taking a multi-pronged approach. Most are “loosening their underwriting standards”[iii] as the overall economy continues to heat up. That can include things like reducing score thresholds or changing debt-to-income (DTI) ratios to offer cards to consumers they may have previously denied.

Another tactic banks are using is increasing the rate and type of card offers they present. During lockdowns, banks shied away from offering travel and rewards cards to avoid coming off as tone-deaf. With the easing of travel restrictions, increasing vaccination rates and a consumer base foaming at the mouth to spend their record savings, banks have resumed presenting travel and rewards to grow new account openings.

Banks have also increased their direct outreach, sending “an estimated 260 million credit-card solicitations in March, up 23% from February and the highest since March 2020.”[iv] But while the volume of offers is up, card issuance is still lagging.

Some of the largest retail banks are also exploring new ways to identify potential card customers who do not have traditional credit files. In a recent announcement, organizations like Wells Fargo, U.S. Bancorp, JPMorgan Chase and others said they will share and evaluate “information from applicants’ checking or savings accounts at other financial institutions to increase their chances of being approved for credit cards.”[v]

The hope is to identify credit-worthy consumers through their account management habits, and provide them with needed credit products. While this represents a significant shift in traditional underwriting tactics, it does hold potential to support the needs of the nearly 53 million underbanked Americans without a traditional credit file.

Tying It All Together

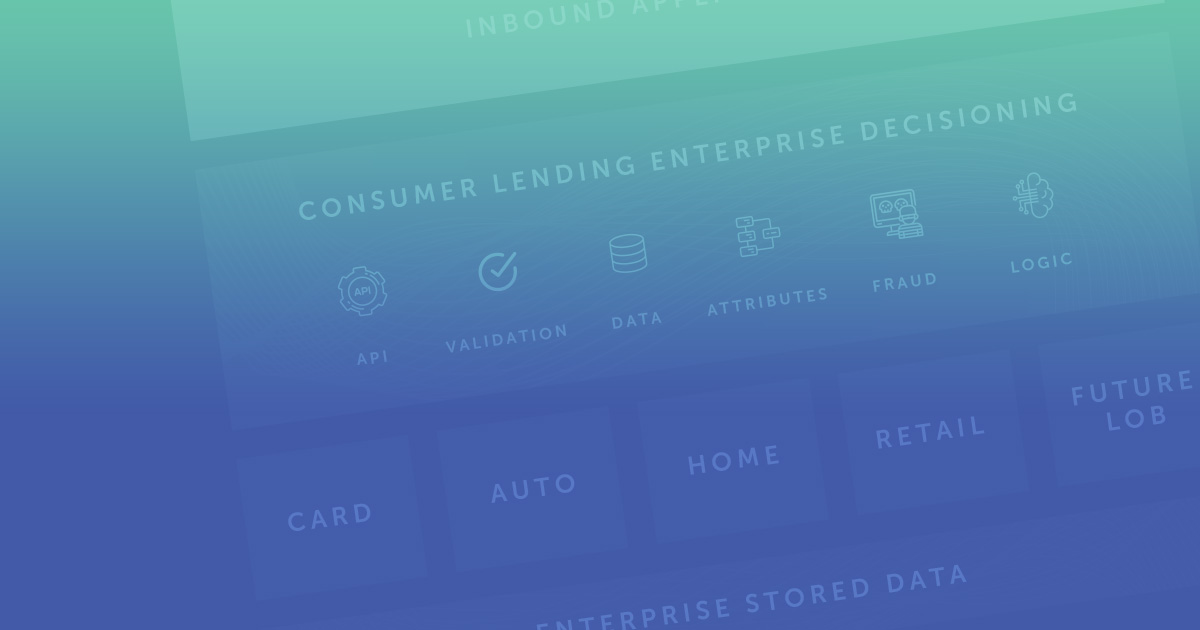

While the outcome of all these ambitious tactics remains to be seen, banks are clearly making changes to bring on new credit card customers. How can they ensure that they are well positioned to take advantage of these changing dynamics? The best approach is to implement a comprehensive, enterprise-class credit card origination system like the one Zoot provides.

Using Zoot’s single, flexible interface, issuers can make immediate changes to criteria like score thresholds and ratios, opening up credit to wider audiences. This can be especially helpful for short-term acquisition initiatives tied to promotions or seasonal offers.

Zoot also enables and encourages users to plug in data from virtually any internal or external source for consideration and inclusion in a credit risk decision. Whether banks are looking at the histories of their own customers, data from other banks or alternative information like utilities payment histories, an origination system from Zoot empowers underwriters to make the right offer to the right person.

Automated decisioning also slashes the time to approval, delivering an exceptional experience at a time when competition is fierce. Zoot provides millisecond processing and decisioning, empowering companies to make instant offers for qualified applicants.

If your organization is ready to improve the card application, underwriting and approval process, putting the right tools in place today will pay significant returns in the future. If you would like to talk about how to make these approaches part of your daily reality, please reach out – we build custom origination solutions every day.